How to Sell Your Startup

While startups are bought—not sold—there are many things you can do as a founder to set your company up for a successful exit. The key is thinking ahead and approaching M&A with the same methodical execution you apply to product development or engineering. Here are the steps to guide you through the process.

1. Decide On Using a Banker

The decision to engage investment bankers for your M&A process depends heavily on your situation. While bankers can handle many steps on your behalf—including building your pipeline and managing negotiations—their involvement may send an unwanted signal to the market. Moreover, it's better to handle the process yourself than work with a subpar banker who will waste time and resources without results. Here's when using a banker makes sense and when it doesn't:

When Bankers Add Value:

- Your company is at Series C or later with significant revenue (>$50M ARR)

- You're running a competitive process with multiple potential acquirers or need help reaching strategic buyers outside your immediate network

- The deal complexity requires dedicated financial modeling and transaction support

When Bankers May Be a Negative Signal:

- You're an early-stage startup (Seed to Series B) where relationships matter more than process

- You already have strong relationships with potential acquirers

- You're in preliminary discussions with a single interested party

If you do decide to use bankers, choose ones with specific expertise in your sector who can add strategic value beyond just running a process. The best bankers bring deep industry relationships and can help position your company effectively.

2. Build Relationships

- Create a list of potential acquirers. Your acquirers tend to fall into a few buckets: larger competitors, partners and customers of your products, and larger companies that are threatened by your competitors. The third bucket, while less obvious, can be one of the most strategic outcomes.

- Start building the relationships with these businesses well before you need to get acquired. Think a year or two. If you only have 3–6 months of cash left you will end up with a fire sale for pennies.

- Make sure you're building the relationships with right decision makers—namely a CEO, GM, or a CXO level executive. Don't waste your time with Corp Dev teams; while they execute on the M&A decision, they don't actually initiate it.

- Consider partnerships that could lead to acquisition.

Make sure to understand what an acquirer can pay. Companies typically spend at most 1-2% of their market cap on an M&A transaction. If your competitor is publicly trading at $8B, $100-$150M is probably the larger end of what they can spend.

3. Start the Conversation

Bringing up an M&A conversation can seem daunting. Here are a few practical steps:

-

Schedule a casual 1:1 coffee or lunch with the potential acquirer's senior executive (not Corp Dev). Frame it as a catch-up or partnership discussion rather than explicitly mentioning acquisition.

-

Share your company's recent successes and growth trajectory (and, if you're partners, share partnership success stories), then naturally transition into discussing how your solutions could complement their strategy further (more on positioning below). When you do broach the topic, keep it exploratory:

-

Use phrases like "exploring strategic options" or "evaluating potential deeper partnerships" rather than directly stating you want to sell.

-

Ask about their build-vs-buy strategy in your space and their thoughts on recent industry consolidation.

-

If you already have interest from another party, say something along the lines of "I value our partnership and wanted you to know we've received some inbound interest from a strategic and/or competitor. We're still in the exploratory phase, but given our relationship, I wanted you to be the first to know, etc." Be prepared to not answer a slew of questions on who the acquirer is and at what price.

Never appear desperate or indicate that you need to sell. The conversation should always position an acquisition as a strategic opportunity for both parties, not a necessity for either side.

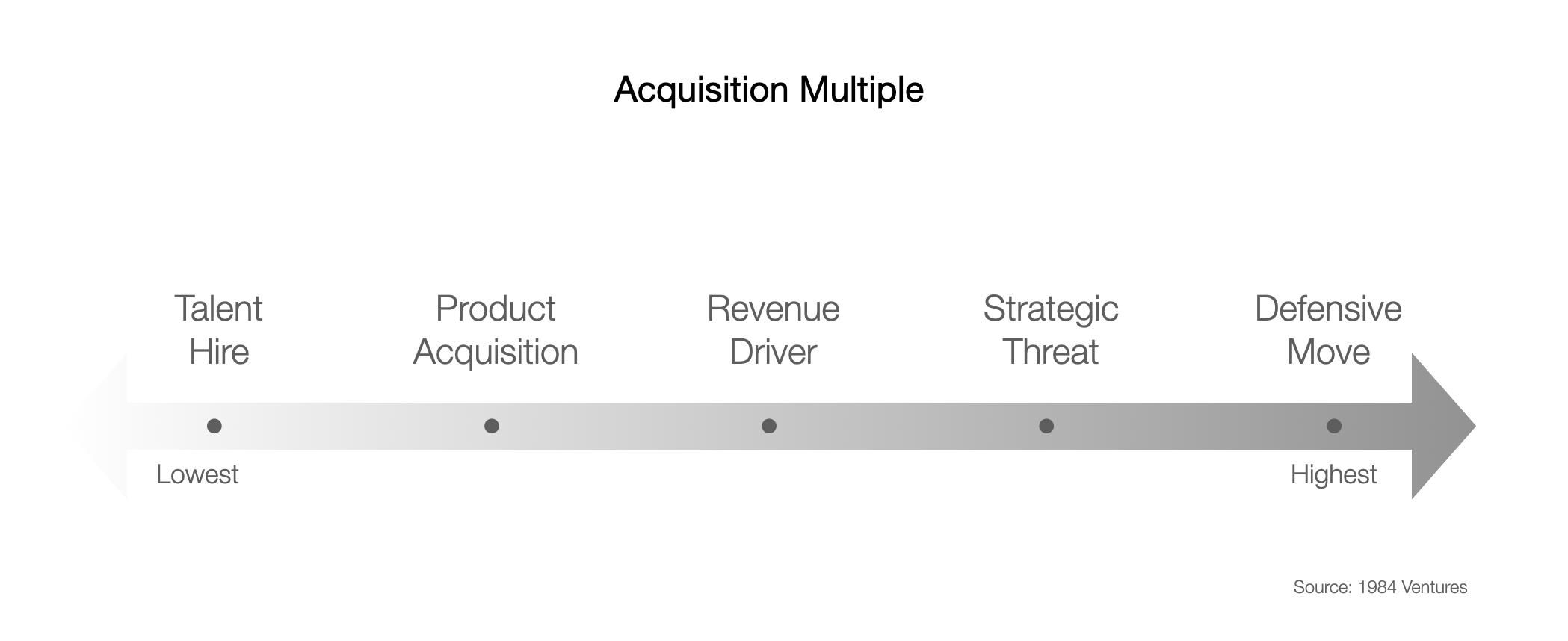

4. Position Your Company Around the Combined Value

Many founders focus too narrowly on their current revenue or product features. However, talent, revenue, or product acquisitions are actually some of the less valuable M&A outcomes. The highest value comes from positioning the acquisition as a strategic threat or a defensive move.

Start by telling a compelling "1+1=11" story - demonstrating how combining your company with the acquirer can create exponential value. For example, highlight how your product could drive massive revenue when distributed through the acquirer's existing customer base, how your technology could transform their core business, or how your team's expertise could accelerate their strategic initiatives. Paint a picture of transformative potential rather than just current metrics.

Start by telling a compelling "1+1=11" story - demonstrating how combining your company with the acquirer can create exponential value. For example, highlight how your product could drive massive revenue when distributed through the acquirer's existing customer base, how your technology could transform their core business, or how your team's expertise could accelerate their strategic initiatives. Paint a picture of transformative potential rather than just current metrics.

If your goal is to be acquired by a large strategic, consider quietly engaging with that company's top competitor. Letting it "slip" that you're in conversation can create a sense of urgency and FOMO. It's a tactical way to drive interest and speed.

5. Understand and Drive the Deal Structure

- In order to both maximize the value and to minimize the time, expense, and frustration that can be associated with the process, you must carefully prepare the company or business for sale, including setting up a dataroom, etc. For more see Legal Consideration for M&A.

- Start thinking about the right structure and whether an asset acquisition, stock acquisition or a full merger is the appropriate structure here. For more on these see Structuring M&A.

- Think about what matters to you beyond just the cash and consideration such as timing of payments, earnouts, title and role, etc. For a comprehensive list of the typical M&A terms see Terms To Negotiate in an M&A Transaction.

- Always get a second bidder.

Once you receive an LOI, immediately prioritize getting a second term sheet to strengthen your negotiating position. Reach out to partners and potential acquirers, informing them that you've received an acquisition offer. Always maintain confidentiality about the potential acquirer's identity, though in some cases you may indicate the general price range or hint at competition.

6. Convince Your Investors

In certain situations, your investors may be hesitant to sell if they perceive the outcome as less favorable than the company is worth. You can use a mix of fear and greed here: fear of your company's outcome as a standalone entity, and greed about the acquirer's stock potential if it's a stock acquisition.

If you have only raised financing through SAFEs, you generally can execute the M&A deal without investor approval since you control the common shares and the board. However, once you have raised a priced round, you typically need both board approval and majority approval from preferred shareholders (i.e., investors) to proceed with the transaction.

This may sound self-serving, but don't screw over your investors. The top VCs won't care if they're getting 1x or 1.5x financially, but they will remember how you handled the process. Be fair. You may need those same investors to vouch for you during your next venture.

7. Post-Deal Considerations

The period between finalizing the term sheet and finalizing the definitive transaction documentation is typically the most demanding phase in the life of the founder, requiring extensive documentation, legal reviews, and detailed integration planning. Expect 4-8 weeks of around the clock work dealing with every detail from a missing NDA for a consultant you hired five years ago to replacing an open source module in your codebase the acquirer deems too risky.

Prepare your team for the transition. Their biggest two questions are how much will I make and is my job secure . Address concerns about job security and changes in company culture. Set expectations about the new operating world. And if the transaction includes layoffs plan for these conversation carefully.

Your team will need your leadership at this stage. Show up for them, explain the decision and lead them through the transition. The acquirer may choose to keep your company's team and culture intact or may chose to totally absorb it. Most acquirers will say the former and end up doing the latter. In either case make sure your team is well integrated into the acquirer and isn't too isolated. It's better for their careers.

Common Pitfalls to Avoid

- Don't neglect your core business during the process. Ideally, only your co-founder should know about the process if you're early-stage (or your CFO and a handful of key people if you're late-stage). This news will spread like wildfire and effectively pause your company's progress.

- Don't wait until you're forced to sell.